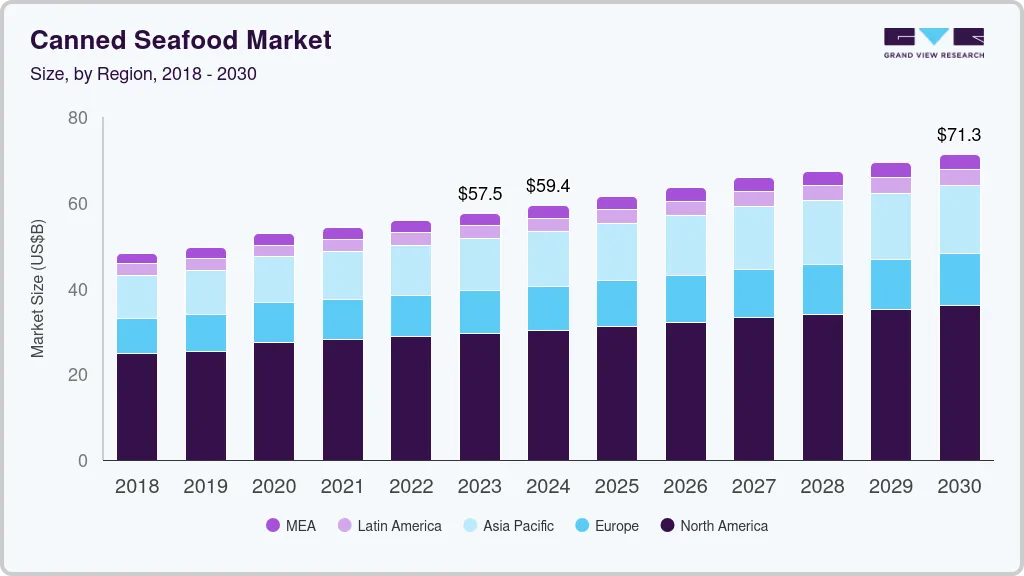

The global canned seafood market size was estimated at USD 35.77 billion in 2024 and is projected to reach USD 44.27 billion by 2030, growing at a CAGR of 3.5% from 2025 to 2030. The rising demand for convenience foods is significantly driving the growth of the canned seafood industry, reflecting broader trends in consumer behavior and market dynamics.

As lifestyles become increasingly fast-paced, consumers are gravitating toward ready-to-eat and easy-to-prepare meals. This trend is especially notable among working populations and younger generations, who often prioritize convenience due to limited time and busy schedules.

The canned seafood market is further supported by advancements in distribution channels that have enhanced accessibility. Supermarkets, convenience stores, and retail outlets remain critical to sales, while the growth of online platforms has allowed consumers to easily purchase products at competitive prices. This convenience has become particularly important in urban regions, where consumers seek to stock up on pantry essentials without frequent grocery store visits.

Sustainability is another key driver shaping the market. Companies are increasingly focusing on eco-friendly packaging and sustainable practices to minimize their environmental footprint. For instance, John West’s EcoTwist packaging reduces steel use and eliminates plastic shrink wrap, cutting down on waste. Moreover, brands are adopting recyclable materials and incorporating traceability features like QR codes, allowing consumers to track product origins. These efforts resonate strongly with environmentally conscious consumers, reinforcing trust and loyalty.

Key Market Highlights:

- Asia Pacific accounted for a share of 35.7% of the global revenue in 2024.

- By product, fish segment accounted for a global market share of 75.3% in 2024.

- By distribution channel, the retail segment accounted for a share of 63.9% of the global revenue in 2024.

Download a free sample PDF of the Canned Seafood Market Intelligence Study from Grand View Research.

Market Performance:

- 2024 Market Size: USD 35.77 Billion

- 2030 Projected Market Size: USD 44.27 Billion

- CAGR (2025-2030): 3.5%

- Asia Pacific: Largest market in 2024

Prominent Companies & Market Dynamics:

The canned seafood market includes numerous domestic and international players. Key participants in the global canned seafood market include StarKist Co., Thai Union Group PCL, Trident Seafoods, LDH (La Doria) Ltd, Wild Planet Foods, and American Tuna, Inc. Established players are investing heavily in research and development to introduce innovative products and sustainable packaging solutions. With extensive distribution networks and strong brand presence, these companies continue to maintain a dominant position in the market.

Key Companies:

- Thai Union Group PCL

- StarKist Co.

- Trident Seafoods

- Tri Marine

- Maruha Nichiro Corporation

- Icicle Seafoods Inc.

- LDH (La Doria) Ltd

- American Tuna

- Universal Canning Inc.

- Wild Plant Foods

Explore Horizon Databook – the world’s most comprehensive market intelligence platform by Grand View Research.

Conclusion

The canned seafood market is experiencing steady growth, fueled by the rising preference for convenience foods, improved accessibility through modern retail and online channels, and an increasing focus on sustainability. With Asia Pacific leading in revenue share and companies innovating to meet evolving consumer expectations, the market is set to expand further. Growing demand for eco-friendly packaging and transparent sourcing practices will continue to drive brand differentiation and consumer trust, ensuring long-term growth for the industry.