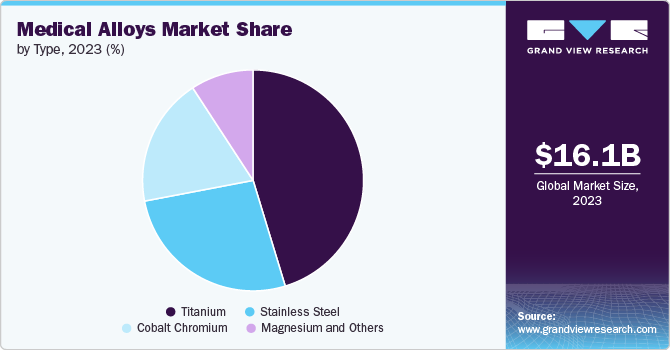

The global medical alloys market size was estimated at USD 16.12 billion in 2023 and is projected to reach USD 28.83 billion by 2030, growing at a CAGR of 8.7% from 2024 to 2030. The market growth is primarily driven by the increasing demand for medical implants, fueled by the rising prevalence of chronic diseases and an aging global population.

Health conditions such as osteoporosis and cardiovascular diseases are accelerating the need for strong, biocompatible materials like titanium and cobalt chromium. These alloys are particularly important in minimally invasive procedures and next-generation implant technologies, which require durability, safety, and high performance.

Technological advancements are further shaping the industry, with innovations such as biodegradable magnesium alloys for temporary implants and advanced cobalt chromium alloys for cardiovascular stents. Ongoing R&D, coupled with continuous product development, is broadening the applications of medical alloys in modern healthcare.

Key Market Highlights:

- North America dominated the global medical alloys market in 2023.

- The U.S. accounted for the largest market share within North America.

- By type, the titanium segment held the largest revenue share in 2023.

- By application, the orthopedic segment led the market in 2023.

Download a free sample PDF of the Medical Alloys Market Intelligence Study from Grand View Research.

Market Performance:

- 2023 Market Size: USD 16.12 Billion

- 2030 Projected Market Size: USD 28.83 Billion

- CAGR (2024–2030): 8.7%

- North America: Largest Market in 2023

Prominent Companies & Market Dynamics:

Leading players are strengthening their portfolios by focusing on high-performance, biocompatible alloys tailored for implants, surgical tools, and medical devices.

- Carpenter Technology Corporation is a global leader in specialty alloys, offering titanium, cobalt chromium, and stainless steel for medical applications. The company focuses on developing corrosion-resistant and biocompatible materials critical for implants and surgical instruments. Its strong R&D capabilities allow it to innovate alloys that meet strict healthcare industry standards.

- ATI Specialty Alloys Components specializes in advanced specialty materials, including medical-grade titanium and other alloys for orthopedic, dental, and surgical applications. Leveraging expertise across aerospace, defense, and healthcare, ATI delivers high-performance alloys designed for precision and reliability.

Key Companies:

- Ametek Specialty Products

- Aperam SA

- ATI Specialty Alloys Components

- Carpenter Technology Corporation

- Fort Wayne Metals

- Johnson Matthey PLC

- Materion Corporation

- Questek Innovations LLC

- Royal DSM

- Supra Alloys Inc.

Explore Horizon Databook – the world’s most comprehensive market intelligence platform by Grand View Research.

Conclusion

The medical alloys market is set for strong growth, supported by the rising demand for advanced implants, the aging global population, and technological innovations in biocompatible materials. With continuous R&D and growing applications in orthopedics, cardiovascular care, and surgical devices, the market offers significant opportunities for expansion through 2030.

No comments:

Post a Comment