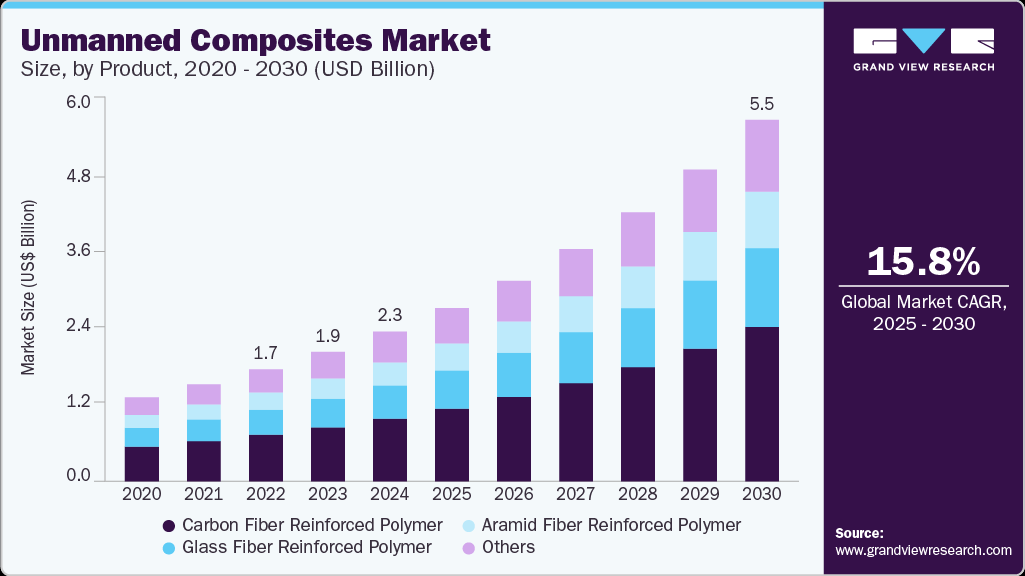

The global unmanned composites market was valued at USD 2.29 billion in 2024 and is projected to reach USD 5.53 billion by 2030, expanding at a CAGR of 15.8% from 2025 to 2030. This market growth is largely driven by the rising preference among unmanned system manufacturers for composite materials, primarily to achieve significant weight reduction.

Additionally, stringent environmental regulations introduced by various governments are encouraging the adoption of lightweight and fuel-efficient unmanned systems. These regulatory trends are expected to further accelerate the demand for composite materials in the sector.

The integration of composites in unmanned systems leads to better overall performance. Ongoing innovations in composite manufacturing techniques are also enhancing system durability and operational efficiency. With their superior strength-to-weight ratio, composite materials contribute to increased fuel economy and lower operational costs—factors that are crucial in the design and development of unmanned platforms.

Key Market Insights:

- North America led the global unmanned composites market in 2024, securing the largest revenue share of 40.6%. This leadership is attributed to substantial defense and security investments, a robust technological foundation, and a rising adoption of unmanned systems in commercial sectors such as logistics, agriculture, and environmental monitoring—collectively contributing to regional growth.

- By product, Carbon Fiber-Reinforced Polymer (CFRP) emerged as the top segment in 2024, accounting for a 41.9% revenue share. CFRP’s dominance stems from its advantageous features, including exceptional strength-to-weight ratio, high stiffness, outstanding temperature and chemical resistance, and minimal thermal expansion.

- In terms of application, the interior segment held the largest revenue share of 61.9% in 2024. Composite materials are extensively utilized in producing interior components such as insulation, panels, structural parts, control surfaces, conduits, seating, and compartments of unmanned systems.

Order a free sample PDF of the Unmanned Composites Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

- 2024 Market Size: USD 2.29 Billion

- 2030 Projected Market Size: USD 5.53 Billion

- CAGR (2025-2030): 15.8%

- North America: Largest market in 2024

Key Companies & Market Share Insights

Key players in the unmanned composites market are actively adopting strategies such as robust investment in research and development, strategic collaborations, supply chain optimization, and advancements in manufacturing processes. These companies are also prioritizing innovation, expanding their product lines, and improving material performance to enhance their competitive edge and meet the evolving needs of the industry.

Among the prominent players in this market are Teijin Ltd., Toray Industries, Inc., PPG Industries, Inc., and Owens Corning.

- Teijin Ltd. offers a diverse portfolio of products and services across sectors such as information & electronics, safety & protection, environment & energy, and healthcare. The company operates globally, with a presence in Europe, Asia, and the Americas. Its business is structured into five key segments: advanced fibers & composites, electronic materials & performance polymer products, healthcare, trading & retail, and others.

- Toray Industries, Inc. is a leading producer and supplier of a wide range of composite materials, including carbon fiber products, thermoset and thermoplastic prepregs, unidirectional tapes, and laminates. These materials are widely used in the production of structural, semi-structural, and interior components for unmanned systems.

Key Players

- Teijin Ltd.

- Toray Industries, Inc.

- PPG Industries, Inc.

- SGL Group

- Hexcel Corporation

- Compagnie de Saint-Gobain S.A.

- Cytec Industries (Solvay, S.A.)

- Renegade Materials Corporation

- Unitech Aerospace

- Gurit

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

In conclusion, the unmanned composites market is undergoing significant transformation as manufacturers increasingly prioritize lightweight, durable, and high-performance materials to meet the evolving demands of modern unmanned systems. Regulatory pressures, technological advancements, and growing commercial applications are further accelerating the shift toward composites. Industry leaders are actively pursuing innovation, strategic partnerships, and advanced manufacturing techniques to stay competitive and address a wide range of defense and civilian applications. As the market continues to mature, composite materials will play a critical role in shaping the future of unmanned systems across the globe.