Medical Equipment Maintenance Industry Overview

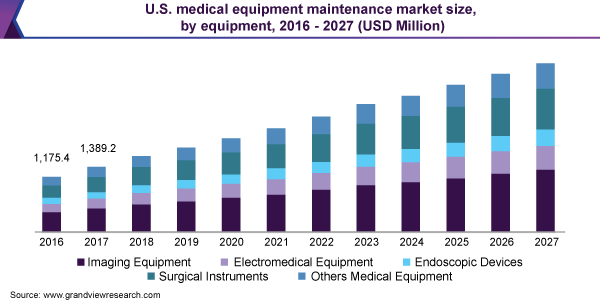

The global medical equipment maintenance market size is expected to reach USD 61.7 billion by 2027, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 7.9% from 2021 to 2027. Rising focus on preventive device maintenance, adoption of advanced funding mechanisms, growth of the associated devices markets, and increasing market share of refurbished medical devices are anticipated to drive the market over the forecast period.

In addition, a surge in the need for technologically advanced medical equipment and an increase in healthcare expenses are expected to propel the market growth. The maintenance of medical devices is a very essential procedure owing to the high use of devices in critical health matters. For instance, calibration is a vital procedure for any medical device to maintain and improve its precision and accuracy, thereby preventing any safety hazards.

Furthermore, increasing global disposable income, rising medical device approvals, and growing adoption of new technologies in emerging countries are projected to further fuel the sales of medical devices, in turn, promoting the maintenance demand. Due to the growing geriatric population, higher expenditure is witnessed for remote patient monitoring devices. And these devices require higher maintenance, which is expected to carry on over the forecast period, thus contributing to the market revenue.

Medical Equipment Maintenance Market Segmentation

Grand View Research has segmented the global medical equipment maintenance market based on equipment, service, and region:

Based on the Equipment Insights, the market is segmented into Imaging Equipment, Electromedical Equipment, Endoscopic Devices, Surgical Instruments, and Other Medical Equipment

- The imaging equipment segment accounted for the largest revenue share of 35.8% in 2020, which includes several devices such as CT, MRI, Digital X-Ray, ultrasound, and others.

- The surgical instruments segment is expected to register the highest CAGR of 8.4% over the forecast period.

Based on the Service Insights, the market is segmented into Preventive Maintenance, Corrective Maintenance, and Operational Maintenance

- The corrective maintenance segment accounted for the largest revenue share of 57.1% in 2020.

- The preventive maintenance segment is anticipated to register the highest CAGR of 8.7% over the forecast period.

Medical Equipment Maintenance Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

Companies are adopting partnership as a key strategy to sustain in the highly competitive environment and acquire a greater market share.

Some prominent players in the global Medical Equipment Maintenance market include:

- GE Healthcare

- Siemens Healthineers

- Koninklijke Philips N.V.

- Drägerwerk AG & Co. KGaA

- Medtronic

- Braun Melsungen AG

- Aramark

- BC Technical, Inc.

- Alliance Medical Group

- Althea Group

Order a free sample PDF of the Medical Equipment Maintenance Market Intelligence Study, published by Grand View Research.