The global vacuum contactor market size was valued at USD 4.52 billion in 2024 and is projected to reach USD 6.65 billion by 2030, expanding at a CAGR of 6.7% from 2025 to 2030. The growing emphasis on industrial energy efficiency and the deployment of smart, modernized grid infrastructure are major factors driving market expansion.

Vacuum contactors play a crucial role in applications involving frequent switching of motors, transformers, and capacitors, particularly in settings that demand arc suppression, equipment reliability, and compact design. As industries strive to minimize downtime and reduce power loss, vacuum contactors are increasingly preferred over traditional air contactors due to their superior arc quenching performance and low maintenance requirements.

The market is further benefitting from global infrastructure modernization initiatives and the integration of renewable energy systems. Countries across Asia-Pacific, especially China and India, are making significant investments in industrial automation and smart grid projects, stimulating regional growth. Additionally, the expansion of mining, oil & gas, and rail infrastructure in emerging economies presents new opportunities for adoption. The rise in urbanization and industrial activity has accelerated energy consumption, prompting industries to focus on improving operational efficiency and energy management. Vacuum contactors, with their ability to reduce power loss and enhance energy utilization, are becoming increasingly vital in achieving these objectives.

Key Market Trends & Insights

- Asia Pacific vacuum contactor market held the largest share of 45.3% in 2024.

- The U.S. market continues to grow due to its strong industrial base and rapid adoption of energy-efficient technologies.

- By application, the motors segment led the market with a 37.8% share in 2024.

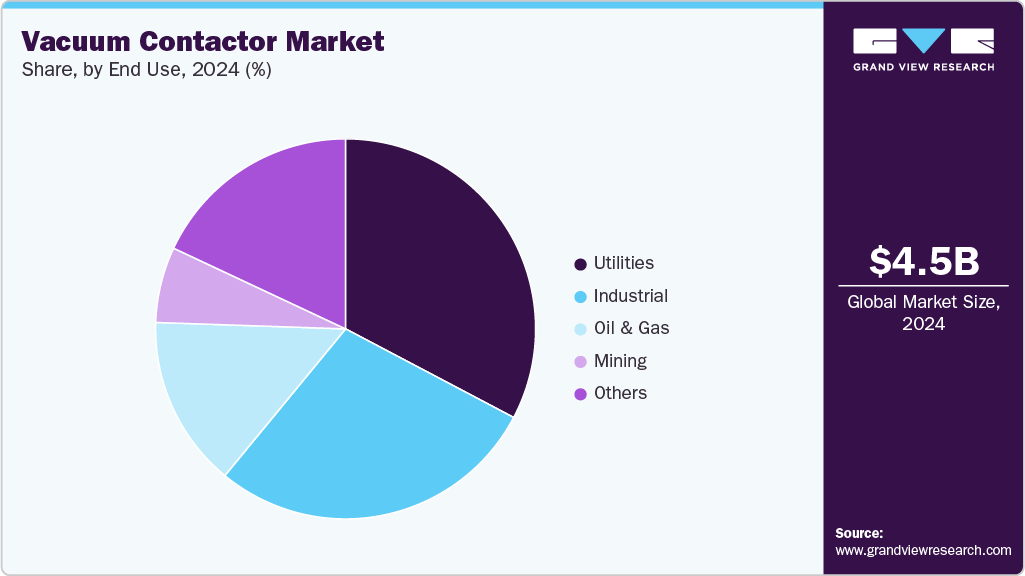

- By end use, the utilities segment dominated and is projected to grow at the fastest CAGR of 7.1% during the forecast period.

Download a free sample PDF of the Vacuum Contactor Market Intelligence Study, published by Grand View Research.

Market Performance

- 2024 Market Size: USD 4.52 Billion

- 2030 Projected Market Size: USD 6.65 Billion

- CAGR (2025–2030): 6.7%

- Asia Pacific: Largest market in 2024

Competitive Landscape

Leading companies operating in the market include ABB Limited, Siemens AG, and TDK Electronics AG, among others.

- ABB Limited is a global leader in power and automation technologies, operating in over 100 countries with a workforce of around 110,000 employees. The company provides innovative products and systems that help customers in utilities, transportation, and industry enhance operational performance and reduce carbon emissions.

- Siemens AG, headquartered in Munich, Germany, is a key player in electrical engineering and electronics. With over 300,000 employees, Siemens serves industries such as manufacturing, healthcare, transportation, and infrastructure, offering solutions that promote energy efficiency and sustainability.

Key Companies

- ABB

- Crompton Greaves Consumer Electricals Limited

- Fuji Electric Co., Ltd.

- Specialty Product Technologies

- Larsen & Toubro Limited

- Rockwell Automation

- Schneider Electric

- Siemens

- TDK Electronics AG

- Toshiba Corporation

Explore Horizon Databook – the world’s most comprehensive market intelligence platform by Grand View Research.

Conclusion

The global vacuum contactor market is poised for consistent growth, supported by the rapid industrial transformation, smart grid advancements, and the ongoing global shift toward energy-efficient technologies.