Tobacco Industry Overview

The global tobacco market size is expected to reach USD 1,049.9 billion by 2030, according to a new report by Grand View Research, Inc. The market is projected to expand at a CAGR of 2.4% from 2022 to 2030. The growing demand from developing nations, coupled with the rising proliferation of next-generation products across the globe is driving the market growth. The high marketing expenditure and product discounts by major tobacco companies are further driving the industry growth.

Consumption of tobacco through cigarettes has been the predominant factor driving the market growth. According to a World Health Organization (WHO) report in 2019, more than 80% of tobacco users live in low- and middle-income countries. Government cessation policies have been unable to help people stop tobacco use. The demand for the product is inelastic, which is expected to drive market growth. The introduction of next-generation products by major manufacturers is another factor expected to fuel the growth.

Tobacco Market Segmentation

Grand View Research has segmented the global Tobacco market on the basis of product, distribution channel, and region:

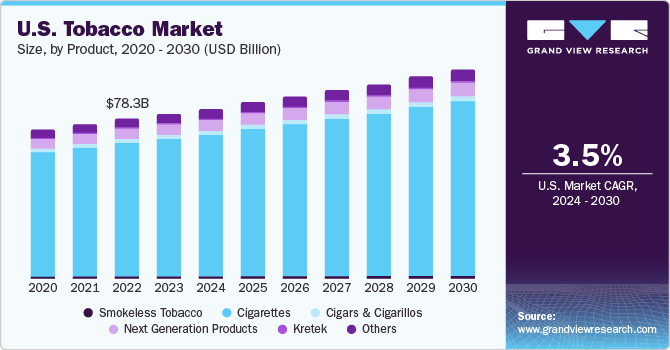

Based on the Product Insights, the market is segmented into Smokeless, Cigarettes, Cigar & Cigarillos, Next Generation Products, and Waterpipes

- Cigarettes captured the majority share of the market in 2021, accounting for nearly 86% of the overall revenue. Cigarette consumption has remained stable due to the introduction of flavored, and menthol cigarettes.

- It can also be attributed to the availability of small cigarettes that facilitate smaller amounts of tobacco consumption for smokers who wish to cut down on their smoking habit.

- Cigarettes have an inelastic demand, which is a major factor that has driven market growth despite the heavy taxation that has been levied across the globe.

- The rising popularity of partying and pub culture among millennials and working-class communities has especially fueled the demand for flavored and unflavored cigarettes around the world in recent years.

- Furthermore, emerging economies such as India and Thailand are seeing a significant increase in cigarette demand as a result of rising youth populations in these countries.

- The tobacco market is expected to benefit greatly from the launch of next-generation products, which is expected to become the fastest-growing segment.

Based on the Distribution Channel Insights, the market is segmented into Offline and Online

- The offline channel led the market and accounted for the largest market share of more than 89% in 2021. It is projected to continue leading the market during the forecast period.

- Consumers prefer these stores as they offer considerable discounts. Location proximity of these stores facilitates immediate demand fulfillment for tobacco consumption, which is also expected to drive the growth of the segment.

- With the COVID-19 outbreak, consumers resorted to purchasing tobacco products online. Countries having strict lockdown laws prohibited citizens from leaving their homes, except for essential reasons. This facilitated the rise of online tobacco shopping.

Tobacco Regional Outlook

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

The market comprises companies with a stronghold on tobacco products and is launching and developing next-generation products.

Some prominent players in the global Tobacco market include:

- Scandinavian Tobacco Group A/S

- Swedish Match AB

- Altria Group, Inc.

- KT&G Corp.

- Imperial Brands

- Philip Morris Products S.A.

- British American Tobacco

- Japan Tobacco Inc.

- China Tobacco.

- ITC Limited

Order a free sample PDF of the Tobacco Market Intelligence Study, published by Grand View Research.