Automotive Aftermarket Industry Overview

The global automotive aftermarket industry size is expected to reach USD 559.9 billion by 2030, according to a new report by Grand View Research, Inc. The market is anticipated to expand at a CAGR of 3.4% from 2022 to 2030. Digitalization of automotive repair and component sales complemented by advanced technology incorporations in the automobile aftermarket component manufacturing is expected to boost the market growth. The surging reception of semi-autonomous, electric vehicles, and hybrid and autonomous cars, in the years to come, is further expected to bolster the demand for new components.

Automotive Aftermarket Segmentation

Grand View Research has segmented the global automotive aftermarket industry based on replacement part, distribution channel, service channel, certification, and region:

Based on the Replacement Part Insights, the market is segmented into Tire, Battery, Brake parts, Filters, Body parts, Lighting & Electronic components, Wheels, Exhaust components, Turbochargers and Others.

- In terms of market size, the others segment dominated the market with a share of 48.7% in 2021.

- The tire segment would be the largest segment in terms of the replacement parts and is anticipated to dominate the market in terms of size.

- The modern age production technology, such as 3D printing of automotive parts, is extensively being deployed by major players in the industry to optimize their production costs, with 3D printing enabling efficient fabrication performance and reduction of emission toxicity.

Based on the Distribution Channel Insights, the market is segmented into Retailers and Wholesalers & Distributors.

- In terms of market size, the retail segment dominated the market with a share of 56.6% in 2021.

- The retail segment is anticipated to dominate the market arena in terms of size by 2030.

- The wholesale and distribution segment would witness relatively fast growth in terms of revenue from 2022 to 2030.

Based on the Service Channel Insights, the market is segmented into DIY (Do It Yourself), DIFM (Do It for Me) and OE (Delegating to OEM’s).

- In terms of market size, the original equipment segment dominated the market with a share of 72.0% in 2021.

- The OE segment is anticipated to dominate the aftermarket arena in terms of size by 2030.

- The DIY segment would witness relatively fast growth in terms of revenue from 2022 to 2030.

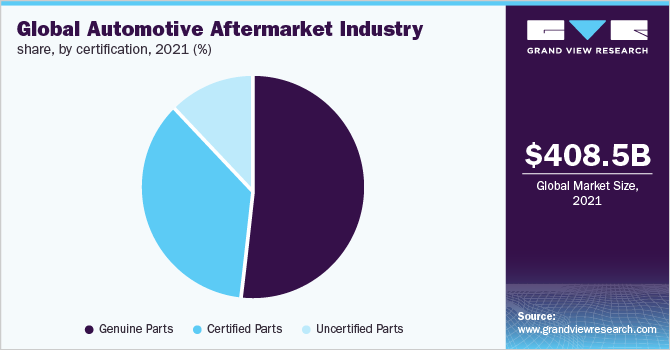

Based on the Certification Insights, the market is segmented into Genuine Parts, Certified Parts and Uncertified Parts.

- In terms of market size, the genuine parts segment dominated the market with a share of 52.0% in 2021.

- The genuine segment is anticipated to dominate the aftermarket arena in terms of size by 2030.

- Uncertified segment would witness relatively fast growth in terms of revenue from 2022 to 2030.

Automotive Aftermarket Regional Outlook

- North America

- Europe

- Asia Pacific

- South America

- MEA

Key Companies Profile & Market Share Insights

Technological proliferation and increasing investments in R&D activities by manufacturers and associations are expected to drive the industry growth. There are numbers of domestic and regional competitors prevailing in the market that are challenged to deliver innovative offerings, which help buyers to address the changing technologies, security needs, and business practices.

Some prominent players in the Automotive Aftermarket include

- 3M Company

- Continental AG

- Cooper Tire & Rubber Company

- Delphi Automotive PLC

- Denso Corporation

- Federal-Mogul Corporation

- HELLA KGaA Hueck & Co.

- Robert Bosch GmbH

- Valeo Group

- ZF Friedrichshafen AG

Order a free sample PDF of the Automotive Aftermarket Intelligence Study, published by Grand View Research.