Minimally Invasive Surgical Instruments Industry Overview

The global minimally invasive surgical instruments market size is estimated to reach USD 60.65 billion by 2030 registering a CAGR of 9.8% from 2022 to 2030 according to a new report by Grand View Research, Inc. The cost of minimally invasive surgical instruments is significantly lower than in patient and open surgeries. Thus, it is beneficial for patients and payers as well. Reduction in healing time, smaller incisions, reduced anastatic use, decreased hospital stays, and increased accuracy has improved its adoption by most surgeons across the globe. Furthermore, an increase in investments by several organizations and hospitals to improve healthcare infrastructure is expected to create opportunities for minimally invasive surgical instrument manufacturers. To deliver a high standard of medical care, surgical wards in newly built hospitals are expected to be equipped with advanced surgical equipment, which is likely to propel market growth in the forecast period.

Minimally Invasive Surgical Instruments Market Segmentation

Grand View Research has segmented the minimally invasive surgical instruments market based on device, end use, application and region:

Based on the Device Insights, the market is segmented into Handheld Instruments, Inflation Devices, Cutter Instruments, Guiding Devices, Electrosurgical Devices, Auxiliary Devices and Monitoring & Visualization Devices.

- In 2021, the handheld instruments segment dominated the minimally invasive surgical instruments market with more than 22% share.

- The handheld instruments market is driven by technological innovations and their growing adoption in minimally invasive surgeries.

- Handheld instruments used in MIS techniques target reducing the amount of damage to extraneous tissues during surgical procedures, thereby speeding patient recovery time and reducing discomfort & side effects.

Based on the Application Insights, the market is segmented into Cardiac, Gastrointestinal, Orthopedic, Vascular, Gynecological, Urological, Thoracic, Cosmetic, Dental and Others.

- The orthopedic application segment dominated the market with a revenue share of over 23.6% in 2021.

- Cardiac surgery is one of the key factors boosting the adoption of minimally invasive surgeries.

- Rising incidence of cardiovascular diseases is one of the significant factors leading to an increase in the adoption of minimally invasive surgeries over conventional ones owing to the various advantages of these surgeries.

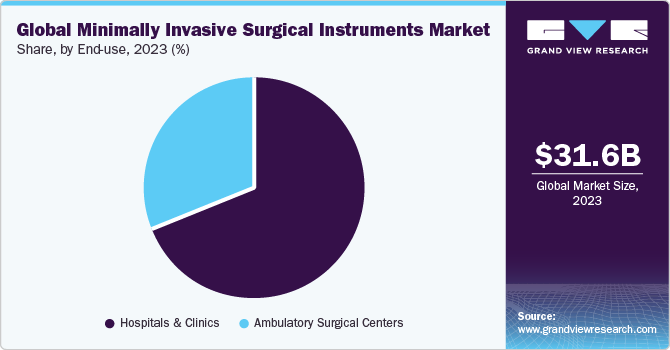

Based on the End Use Insights, the market is segmented into Hospitals and Ambulatory Surgical Centers.

- The hospital segment accounted for the maximum revenue share of over 66.2% in 2021.

- On the other hand, ambulatory surgical centers are expected to witness the fastest growth rate over the forecast period.

- The demand for outpatient surgeries is likely to grow dramatically in the coming years.

- The growth in ambulatory surgical centers can be attributed to several factors including rise in minimally invasive procedures, advancement in the field of anesthesia, enhanced patient experiences, legislative changes, and economic pressures.

Minimally Invasive Surgical Instruments Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Key Companies Profile & Market Share Insights

The global minimally invasive surgical instruments market witnesses a highly competitive market due to the presence of leaders. Most of their revenue is invested in R&D to develop highly interactive technology to strengthen its market position.

Some prominent players in the Minimally Invasive Surgical Instruments market include

- Medtronic,

- Siemens

- Healthineer AG,

- Ethicon, Inc. (Johnson & Johnson)

- Depuy Synthes,

- GE Healthcare

- Abbott Laboratories

- Intutive Surgical Inc.

- Nuvasive Inc.,

- Zimmer Biomet

Order a free sample PDF of the Minimally Invasive Surgical Instruments Market Intelligence Study, published by Grand View Research.

No comments:

Post a Comment