Furfuryl Alcohol Industry Overview

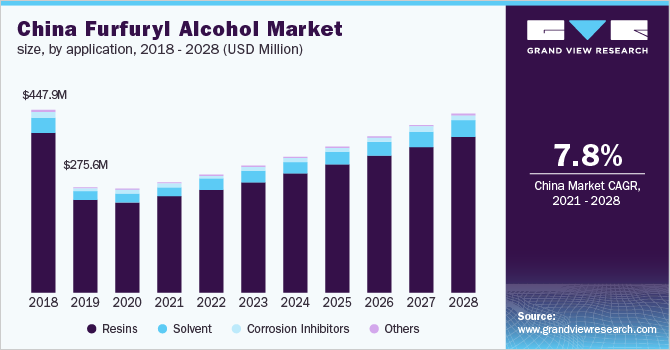

The global furfuryl alcohol market size is estimated to reach USD 821.6 million by 2028, according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 7.2% from 2021 to 2028. Factors such as rising demand for furfuryl alcohol resins from the construction and automotive sectors are expected to drive the market in the near future.

The product has witnessed high demand over the past decade, owing to its growing usage in the foundry, agriculture, and construction industries, among others. The product is broadly utilized in resins and plastics applications. A surge in research and development activities in the area of rocket fuel is estimated to trigger the demand. The products also play an essential role in manufacturing in the foundry sector in the formulation of molds for metal casting.

Furfuryl Alcohol Market Segmentation

Grand View Research has segmented the global furfuryl alcohol market on the basis of application, end-use, and region:

Based on the Application Insights, the market is segmented into Resins, Solvent, Corrosion Inhibitors, and Others.

- The resins application segment dominated the market for furfuryl alcohol and accounted for the largest revenue share of more than 87.0% in 2020. This is attributed to the growing demand for furfuryl alcohol resins from the construction and automotive sectors.

- The surge in demand for low volatile organic compounds (VOC) and non-toxic solvents in agricultural formulations, petroleum refining, pharmaceuticals, paints and coatings, and several other end-use industries is anticipated to fuel the growth of the market for furfuryl alcohol over the forecast period.

- Increasing awareness about the effectiveness of the product as a corrosion inhibitor coupled with its surging demand as an inhibitor in cement, grout, and mortar is expected to trigger market growth in the near future.

Based on the End-use Insights, the market is segmented into Foundry, Agriculture, Paints & Coatings, Pharmaceuticals, Food & Beverages, and Others.

- The foundry end-use segment dominated the market for furfuryl alcohol and accounted for the largest revenue share of more than 82.0% in 2020. This is attributed to the surge in metal casting production.

- The expanding agricultural sector along with the surge in farm production in countries such as China, India, Indonesia, Russia, France, and Germany are expected to fuel the demand for furfuryl alcohol in these economies over the forecast period.

- The growth of the paints & coatings sector in countries that are among the top producers such as Germany, India, and Japan are anticipated to fuel the product demand.

Furfuryl Alcohol Regional Outlook

- North America

- Europe

- Asia Pacific

- Central & South America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

Market participants focus on third-party agreements with professional distributors and also sell distribution rights to these merchants in order to reach developed markets. Key manufacturers have in-house research and development laboratories for analysis of finished products, semi-finished products, and raw materials. Manufacturers are inclined toward collaborations with key players, research institutes, and universities to obtain durable bio-based solutions. Companies are expected to focus on forward integration to reduce logistics & operational costs and acquire a higher market share.

Some of the prominent players in the furfuryl alcohol market include:

- ILLOVO SUGAR AFRICA (PTY) LTD.

- Linzi Organic Chemical Inc. Ltd.

- TransFurans Chemicals bvba

- DalinYebo

- Hebeichem

- p.a.

- Shandong Crownchem Industries Co., Ltd.

- Hongye Holdings Group Corp., Ltd.

- Xian Welldon Trading Co., Ltd.

- Furnova Polymers Ltd.

- NC Nature Chemicals

Order a free sample PDF of the Furfuryl Alcohol Market Intelligence Study, published by Grand View Research.