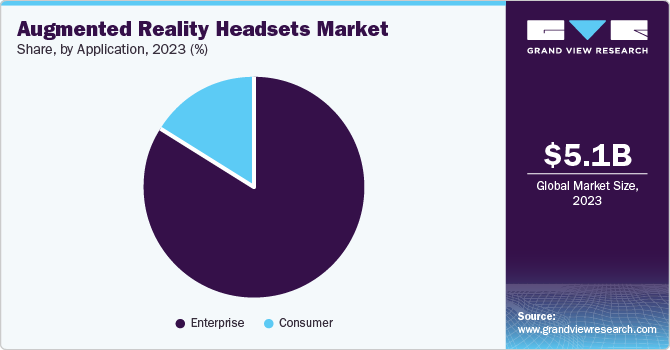

The global augmented reality headsets market size was valued at USD 5.13 billion in 2023 and is projected to reach USD 44.65 billion by 2030, growing at a CAGR of 37.4% from 2024 to 2030. The market is witnessing rapid expansion due to increasing investments, the adoption of AR technologies across multiple sectors, and continuous technological advancements.

Rising funding is driving innovation, enabling the development of more advanced and user-friendly AR headsets. The growing use of AR in industries such as education, healthcare, and entertainment is broadening the market’s scope and boosting consumer interest.

Technological progress in display, sensors, and processing capabilities is enabling more sophisticated and immersive AR experiences. Expanding applications across gaming, entertainment, and enterprise solutions, including manufacturing and healthcare, are further driving market potential. Established tech companies and startups are investing significantly in AR research and development, enhancing user experiences through improved headset comfort, functionality, and immersive features. These factors position AR headsets as essential tools for both professional and personal use, supporting strong market growth. Additionally, rising consumer demand for interactive and engaging experiences is fueling adoption.

AR headsets allow users to perceive real-time interactions with objects in their surroundings using cameras and sensors. Consequently, industries such as education, healthcare, entertainment, and retail are integrating AR to deliver real-life 3D immersive experiences. The increasing trend of overlaying virtual objects on the physical environment is expected to drive product demand. For example, the Microsoft HoloLens enables users to interact with products and access analytical information during trials, enhancing both efficiency and engagement.

Key Market Highlights:

- North America dominated the AR headsets market with a revenue share of 38.9% in 2023.

- Within North America, the U.S. accounted for 82.9% of the regional market in 2023.

- By product, standalone headsets led with a revenue share of 49.1% in 2023.

- By application, the enterprise segment was the largest contributor in 2023.

Download a free sample PDF of the Augmented Reality Headsets Market Intelligence Study from Grand View Research.

Market Performance:

- 2023 Market Size: USD 5.13 Billion

- 2030 Projected Market Size: USD 44.65 Billion

- CAGR (2024-2030): 37.4%

- North America: Largest market in 2023

Prominent Companies & Market Dynamics:

Key players in the AR headsets market include Google LLC, Magic Leap, Inc., Microsoft, VUZIX, Seiko Epson Corporation, RealWear Inc., and others. Companies are actively expanding their customer base and gaining a competitive edge through strategic initiatives such as partnerships, mergers, and acquisitions.

- Google LLC, a subsidiary of Alphabet Inc., operates in advertising, search, Google Maps, Google Docs, Chrome, Google Photos, and hardware in the mixed reality, virtual reality, and AR markets.

- Magic Leap, Inc. leverages scalable production, optics, and AI technologies to deliver immersive AR experiences. The company has developed numerous patents covering key aspects such as projectors, eyepieces, headsets, waveguides, manufacturing processes, and related technologies.

Key Companies:

- Google LLC

- Magic Leap, Inc.

- Microsoft

- VUZIX

- Seiko Epson Corporation

- RealWear Inc.

- Kopin Corporation

- Sony Corporation

- Virtuix

- Niantic

- Meta

- YORD

- Groove Jones, Inc.

Explore Horizon Databook, the world’s most comprehensive market intelligence platform by Grand View Research.

Conclusion:

The augmented reality headsets market is poised for exponential growth, driven by technological advancements, expanding enterprise applications, and rising consumer demand for immersive experiences. Investments in R&D, coupled with innovations in design, comfort, and functionality, are transforming AR headsets into essential tools across industries and personal use, signaling a strong market trajectory.