Predictive Dialer Software Industry Overview

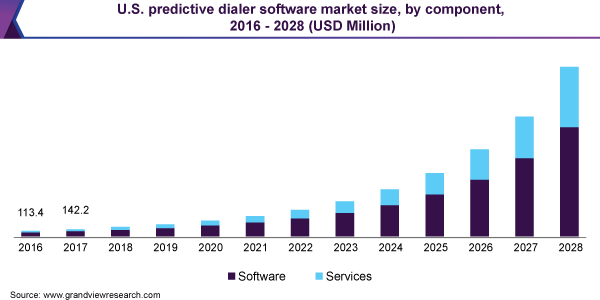

The global predictive dialer software market size is expected to reach USD 12.19 billion by 2028, according to a new report by Grand View Research, Inc. It is expected to expand at a CAGR of 37.0% from 2021 to 2028. Predictive dialer software uses statistical algorithms to predict the availability of contact center agents and estimates the normal time for phone calls to be answered. The dialing rate is then adjusted accordingly considering these two factors.

Businesses are widely adopting predictive dialer systems to reach out to a large number of customers automatically. Furthermore, predictive dialer dials from a list of phone numbers and can detect disconnected phone numbers, voicemail messages, busy signals, and unanswered numbers. Such a system potentially allows companies to keep their customers updated about a service issue or emergency.

Predictive Dialer Software Market Segmentation

Grand View Research has segmented the global predictive dialer software market on the basis of component, deployment, enterprise size, end use, and region:

Based on the Component Insights, the market is segmented into Software and Services.

- The software segment dominated the market in 2020 and accounted for a revenue share of more than 68.0%.

- The services segment is anticipated to witness the fastest growth over the forecast period.

- The services segment has been further segmented into integration and deployment, support and maintenance, training and consulting, and managed services.

Based on the Deployment Insights, the market is segmented into Cloud and On-premise.

- The on-premise segment dominated the market in 2020 and accounted for a revenue share of more than 55.0%.

- The cloud segment is expected to witness the fastest growth over the forecast period. The growth can be attributed to the growing adoption of cloud-based software by businesses to eliminate the hassles and expenses associated with managing an on-premise system.

Based on the Enterprise Size Insights, the market is segmented into Large Enterprises, and Small & Medium Enterprises.

- The large enterprises' segment dominated the market in 2020 and accounted for a revenue share of more than 54.0%.

- The adoption of predictive dialer software for cold-calling and inside sales and customer support activities is growing continuously.

- The software can benefit large enterprises as it is typically designed to handle a large number of customers’ calls in a very short period of time.

- The small and medium enterprises segment is anticipated to witness the fastest growth over the forecast period.

Based on the End-use Insights, the market is segmented into BFSI, Government, Healthcare, IT & Telecom, and Others.

- The IT and telecom segment dominated the market in 2020 and accounted for a revenue share of more than 27.0%.

- The government segment is anticipated to register the fastest CAGR over the forecast period. The growth can be attributed to the growing need for rolling out efficient public services. Government agencies are widely adopting predictive dialer systems to provide quality services to the public.

Predictive Dialer Software Regional Outlook

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa (MEA)

Key Companies Profile & Market Share Insights

The market is highly fragmented in nature. Prominent market players are adopting various strategies, such as strategic joint ventures, partnerships, product innovation, research & development initiatives, geographical expansion, and mergers & acquisitions to cement their foothold in the market. Businesses are focusing on providing both cloud-based and on-premise software solutions to large enterprises. These solutions are designed to help enterprises efficiently manage the high-volume and high-touch automated multichannel campaigns.

Some prominent players in the global predictive dialer software market include:

- Agile CRM

- ChaseData Corporation

- Convoso

- Five9, Inc.

- NICE inContact

- PhoneBurner

- RingCentral, Inc.

- Star2Billing S.L.

- VanillaSoft

- Ytel Inc.

Order a free sample PDF of the Predictive Dialer Software Market Intelligence Study, published by Grand View Research.